Wind in the Sails to Net Zero

Recognizing the importance of minimizing its environmental impact, the maritime industry is at the forefront of intensifying efforts to reduce its carbon footprint.

As a critical cornerstone of global commerce, maritime transport connects the world and facilitates economic growth and development. Recognizing the importance of minimizing its environmental impact, the industry is at the forefront of intensifying efforts to curb its carbon footprint. This paper provides an overview of the key themes to the maritime industry’s decarbonization journey as well as the future advancements that are expected to significantly enhance the industry’s ‘green’ profile. Greenheart believes the initiatives discussed will positively shape the future trajectory of climate change and fundamentally impact why, and how, investors can and should take advantage of the unique opportunities emerging from this period of strategic innovation.

Overview

The Net Zero Asset Owners Alliance (UN-convened group of influential institutional asset owners and stakeholders) has identified shipping as a priority sector and has chosen to actively engage with the maritime industry to encourage thoughtful investment in the existing asset base, nascent technologies, and operating practices, working towards the ultimate goal of a carbon neutral supply chain.

The maritime industry is a vast opportunity set for investors and is the backbone of global commerce, which demands strategic engagement from the entire commercial ecosystem – both industry stakeholders and financial investors seeking to contribute towards tackling these ambitious decarbonization targets.

The asset base consists of ~60,000 deep-sea vessels with an estimated value of $1.4+ trillion. The industry is responsible for the transportation of ~90% of the world’s commodities and finished goods (with an annual value of ~$14 trillion) while producing ~3% of global greenhouse gas (‘GHG’) emissions (equivalent to ~1 billion tonnes of carbon dioxide).

Transportation by sea is the most effective mode of scalable transport per carbon unit, however, substantial improvements are necessary. While there are significant challenges involved in the decarbonization of the maritime industry, there are also opportunities to be gained from, and in many respects, the maritime industry is leading other sectors in its ambitions.

The Importance of Decarbonizing Maritime

As mentioned earlier, the maritime industry accounts for approximately 3% of global greenhouse gas emissions. As the world fleet continues to expand, emissions could grow significantly without meaningful mitigation efforts. Pressure is intensifying on the industry to reduce emissions and contribute to the international goal of net-zero carbon emissions by 2050, despite the unprecedented potential cost, and operational and technological complexities.

From 2012 to 2018, the seaborne fleet grew by 11%, and CO2 emissions increased by just over 9% with annual consumption of marine fuel estimated at circa 300m tonnes. With the fleet expected to continue to grow, marginal changes to CO2 emissions will not be enough in the long term to ensure the sustainability of the industry, and in this context, the decarbonization of shipping is both critical

and incredibly complex.

Developing viable carbon-neutral marine fuels and related propulsion technology, as well as the corresponding need for considerable investment in global supply chain infrastructure, requires coordination and collaboration from all market participants.

Risks of potential first mover disadvantage must be mitigated via appropriate regulatory and governmental incentives to ensure bold initial steps. In addition to asset owners, such action must ultimately come from both regulatory bodies and end users of the goods and commodities transported including energy majors, national energy and mining firms, and steel and finished goods manufacturers. End-users, such as Cargill, Glencore, Maersk, and Shell, are ultimately the demand that drives vessel usage, and they must play a pivotal role in driving change by taking responsibility and supporting ambitious investments in nascent technologies.

From a regulatory perspective, the IMO is the UN body that, on a global basis, governs the shipping industry. It has set a target of reducing the industry’s total GHG emissions by at least 50% by 2050,

whilst at the same time reducing the average carbon intensity (CO2 per tonne-mile) by at least 40% by 2030, and 70% before 2050. To support this target, it has introduced short-term asset efficiency

measures (EEXI and CII further explained below) to be implemented in 2023 onwards.

Success and actual change will require a realistic but ambitious approach (essentially a dual-track process), meaning that whilst striving towards long-term all-encompassing solutions, the industry must also focus on the current actionable solutions to ensure immediate improvements. Decarbonizing the maritime industry requires substantial research to identify those zero-carbon initiatives with the greatest potential impact to address current key challenges such as operational efficiency, sustainability of resources, the safety of life at sea, storage and bunkering infrastructure, and the cost-effectiveness of new technologies.

Practically speaking, the ultimate goal of zero-emission vessels that are built to a longer lifecycle model and that utilize “green” steel (steel produced with the lowest emissions currently possible) and engineering, needs to be balanced with immediate and sizeable investment programs focused on retrofitting existing assets, a process which makes existing assets more adaptable to evolving technologies. In addition, pilot projects to encourage research and development (R&D) towards future solutions such as bridge fuels, carbon tax, and green corridors (explored below) are all needed to support the pioneers, and both encourage and reward risk-taking.

As was seen at COP26, the November 2021 UN Climate Change Conference, despite good intentions, changing legislation can be incredibly challenging. On this basis, prominent visionaries within the shipping industry are taking the lead on several initiatives. One organization driving such change is the Global Maritime Forum, which is the driving force behind the ‘Getting to Zero Coalition’ initiative, a powerful alliance of more than 160 companies within the maritime, energy, infrastructure, and finance sectors, supported by key governments and intergovernmental organizations. The coalition is committed to getting commercially viable deep sea, zero-emission vessels powered by zero-emission fuels into operation by 2030 – maritime’s moon-shot ambition.

Key Themes to Address in the Maritime Decarbonization Journey

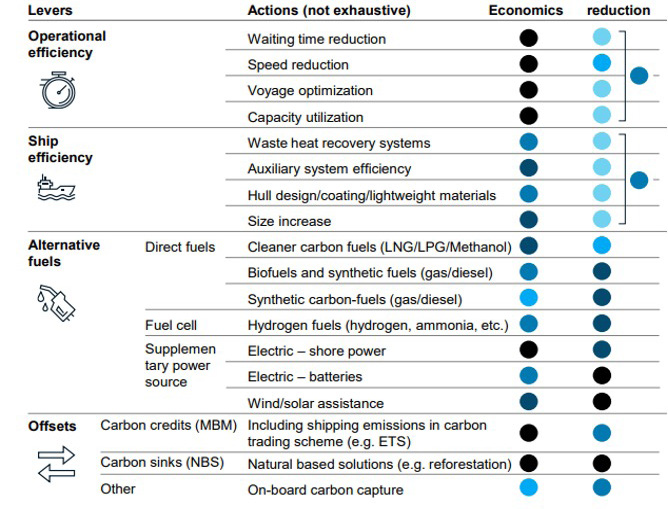

Like many other industries, much of what is required to decarbonize vessels relies heavily on the speed and quality of research and development, in areas such as alternative fuel development and new technologies designed to improve a vessel’s operating performance. However, critical steps can be taken today to move closer to longer-term ambitions. Operational changes within ports such as reducing the waiting time of ships can also have a positive impact on energy usage. These improvements, coupled with a regulatory push, such as the introduction of zero-emission maritime routes (so-called ‘green corridors’) at COP26, mean the maritime industry is moving towards a new future, presenting both opportunities and challenges alike.

The transition towards a net zero supply chain will take decades and there is currently no single solution. In addition to embracing future technology and new operating models, optimizing the existing asset base is a responsible and resourceful path toward reducing the carbon footprint now.

As the transition to net zero occurs, there are meaningful further steps vessel owners can implement to reduce their GHG impact.

- Retrofitting to enhance performance is an actionable initiative with quantifiable results, reducing fuel consumption and lowering GHG emissions.

- It is estimated that the construction process of a Newbuild vessel has a 40-50% higher carbon footprint than an existing vessel’s annual emission footprint. Therefore, before viable new propulsion technologies are widely adopted, retrofitting existing vessels, in some instances is a more environmentally friendly approach.

- Further improved technologies include high-specification silicon-based paint, propellor ducts, waste heat recovery systems, power caps, and voyage optimization technologies that can provide an immediate improvement in the performance of between 2-8% with similar reductions in CO2 emissions.

- Back to the future – the use of modern sails and rotor sails to assist propulsion can be an effective method of reducing fuel consumption (predicted up to 15% improvement), although not applicable to certain vessels and sizes due to operational constraints.

- ‘Air lubrication’ systems can be installed on certain vessels, emitting a thin layer of bubbles from the hull of the vessel to minimize resistance and reduce fuel consumption. This was broadly seen as an ineffective technology a decade ago but has recently gained traction with larger assets and has been vetted and approved by some of the largest energy majors. Claims of up to 20% performance improvement are made by suppliers.

- In the short-term, realizable near-term gains can be achieved and can provide savings in CO2 emissions: voyage optimization (~5%); waste heat recovery (~2%); propellor modification (~5-8%) or hull coatings/lubrication (~5-8%).

- Vessel operational improvements include satellite communications, live weather, and routing data and systems available on vessels to base voyage routes on this data to achieve the most efficient and effective route/speed for vessels.

Greenheart Management’s Emission Reduction Objectives

Greenheart Management and owner Hayfin is a member of the Global Maritime Forum and is a signatory of the ‘Getting to Zero Coalition’ initiative. While the initiative has a long-term vision, Greenheart has proactively established an optimization framework to drive reductions in fuel consumption and lower greenhouse gas emissions that it is putting in action today. Our framework hinges on clear alignment and active partnerships with top-tier charterers to invest in asset enhancements and conduct business in a responsible environmental manner. To this end, Greenheart has implemented near-term solutions such as the retrofitting of secondhand vessels and the utilization of cutting-edge technologies on newbuild vessels. Several examples include, but are not limited to:

Asset capacity surveys to assess the potential for an increase of a vessel’s deadweight tonnage (“DWT”) through minor vessel modifications – adding cargo capacity and thereby reducing CO2 emissions per unit cargo, as more tonnes are carried per nautical mile, which yields a lower Carbon Intensity Indicator (“CII”).

Coating a vessel’s hull with new, anti-fouling silicone-based paints, thereby decreasing the required cleaning and increasing energy efficiency by up to 6% (c. 1,440 tonnes of carbon saved annually).

Air lubrication systems create a carpet of air under the vessel, leading to reduced water resistance. This drives a fuel consumption reduction of 5-8% (c. 1,440 tonnes of carbon saved annually).

Improve the hydrodynamics of vessels by retrofitting devices to improve water flow around the propellor – through the post-swirl duct or pre-swirl duct and/or propellor modification – these options provide fuel savings of up to 8% (over 2,000 tonnes of carbon saved annually).

To benchmark and measure these improvements, we seek to monitor key performance indicators within our fleet such as targeting a vessel performance improvement of 6.0% or more per annum, equal to a reduction of ~1,500 tonnes CO2 per asset, by the completion of the first drydocking post-vessel acquisition; target 1-2% fuel reduction per annum, equating to 270-550 tonnes of CO2, by improving operational and technical performance onboard vessels.

Ultimately, in addition to their significant reduction in emissions, Hayfin believes that these enhancements make critical business sense and will translate into improved asset economics by ensuring our Hayfin Maritime asset base is preferred in all trading scenarios – both protecting the downside (by enhancing utilization and performance) and best positioned for optimal upside (both via generation of cash flow from top tier counterparties and also for an eventual exit).

Operational Improvements and Automation

Further to the improvement that can be made on a bottoms-up (i.e., vessel by vessel) basis, the maritime industry can implement top-down improvements via adjustments to their operating model and automation.

The current contractual framework for the transport of goods by sea encourages the ship owner to “sail fast then wait” (SFTW) to discharge, which results in reduced utilization of ports, increased costs as well as higher emissions. Just-in-time delivery is an inventory management strategy that reduces materials

held in stock by delivering items at the time they are needed for sale. It would be a cheap and quick win to change to just-in-time, from the current SFTW. Academic research suggests that eradicating SFTW and introducing just-in-time practices, which are widely adopted in supply chains, would result in emissions savings in the order of 20-25%. This is equivalent to ~200+ million tonnes of CO2 per year.

Digitalization has become a major topic within shipping with increased automation on ships supporting the optimized operation of vessels and equipment. The use of drones for physical inspections and digital communications between ships and shore-enhancing efficiencies and response times while supporting

decarbonization.

The use of onboard, strategically positioned monitoring equipment, and live transmission of these data points support continuous analysis and optimization of performance. In addition, the use of big data (data sets too large are analyzed through traditional data-process methods), artificial intelligence and machine learning is increasingly being piloted with cloud-based predictive maintenance systems, providing real-time insights detecting failures, prescribing maintenance actions, supporting

asset reliability and optimization of maintenance costs and reduction of the total cost of ownership – optimizing asset performance and reducing fuel consumption.

Future Advancement Hinges on R&D, New Manufacturing Processes and Technologies

As the sector focuses on how to address decarbonization, As the sector focuses on how to address decarbonization, it is concentrating efforts on the advancement of fuel and technology offerings in order to reduce emissions – ‘thinking big, starting small and scaling fast’ in areas such as hydrogen and ammonia research and development, as well as renewable technologies. This new phase of transition will require significant upgrades and modifications to the entire supply chain infrastructure for

maritime assets – vessels, ports, and operations.

Dual Fuel Technology

- The use of liquified natural gas (‘LNG’) and liquified petroleum gas (‘LPG’) in so-called “dual fuel” newbuild vessels is seen as an intermediate step as LNG emits 25% less CO2 and near-zero sulfur oxides and nitrogen oxides, the two main pollutants from a ship’s emissions, compared to conventional fuels. A significant portion (32%) of the current shipyard orderbook is set to use dual fuel technologies.

- Technology is key in the decarbonization journey and apart

from having an immediate impact, some of these bridge fuels can help prepare for permanent solutions both based on increased knowledge and vessels being prepared for other ways to store fuel. - As an example, the LNG fleet has experienced a technology revolution since 2010. Up to 2009, most of the fleet used a steam propulsion system. However, new technology on LNG vessels has seen the development of modern engines and propulsion systems, representing now 11% of the total fleet and the majority of the shipyard orderbook (132 vessels). These modern engines are more efficient, consuming 44% of the fuel of previous engines while complying with current emission regulations.

- Longer term, LNG is not deemed to be a conclusive solution since it is still a fossil fuel and methane emissions are still a major concern. Indeed the “Global Methane Pledge”, recently signed by 100+ nations during COP26, aims to reduce methane emissions by 30% (from 2020 levels) by 2030.

- Shipping propulsion technology has evolved over the last several hundred years from the use of wind power originally, to coal and most recently, combustion and diesel engines. The changes required to decarbonize the industry over the coming decades are a fourth propulsion revolution.

Alternative Fuels

- An industry-financed $5 billion program, to be conducted by a new International Maritime Research and Development Board (IMRB), is currently being considered by governments aimed at accelerating the introduction of zero-emission technologies for maritime transport.

- Methanol, ammonia, and hydrogen may be deployed as fuel for use in an internal combustion engine or in fuel cells. Sustainable biofuel is available for deep-sea shipping with the potential to reduce GHG emissions. Batteries have also been considered although these are only feasible for ferries and short-sea shipping. Currently, 1.8% of the global orderbook uses other alternative fuels.

- Test pilot schemes are ongoing with a focus mainly on green ammonia (CO2 emission-free ammonia from renewable electricity) and green hydrogen (hydrogen produced by splitting water using electricity generated from renewable sources) fuel cells, which are seen as the most promising technologies that achieve net zero GHG emissions.

- Most hydrogen produced globally is derived from fossil fuels and is not considered ‘green’. It is expected that the cost of green hydrogen production will fall to a third of the cost by 2025. However, hydrogen requires large storage volumes, which makes it an unlikely option for long-haul shipping.

- Ammonia is one of the best and most realistic options for emission-free marine fuel. Ammonia has the key benefit of being easier to store than hydrogen. Hence, storage costs are significantly cheaper than hydrogen, electric batteries, or LNG. The difficulties with ammonia are centered around its toxicity and limited experience as a fuel in combustion engines and low energy utilization rates. With a lower energy conversion efficiency than fuel oil, energy density is half that of diesel, hence ammonia producers would need to provide twice as much liquid ammonia. Current production can only cover a moderate fraction of the demand for marine fuels. Current renewable ammonia price ranges from 1.2 to 1.5 times other, more emissions-intensive options.

- Prices for renewable electricity are expected to decrease over time to some extent, allowing ammonia to become more competitive.

- Of the future potential green fuels, ammonia and hydrogen address emissions challenges. However, fuel quality and safety standards need to be developed further for ammonia, while hydrogen storage constraints may be an inhibitor for long-haul shipping.

Carbon Capture and Renewable Assets

- Carbon capture is a process whereby CO2 is captured and stored before it enters the atmosphere, avoiding environmental damage. This concept can be adapted to the maritime environment, for example through recycling of wasted energy within vessels and using this to capture the CO2 from the emissions of a vessel. A critical topic under research is the storage of CO2 on board (feasibility, volume required, safety considerations) and the eventual removal of the captured CO2 (shore-based supply chain and infrastructure in ports).

- Projects around transportation of captured carbon are being assessed and purpose-built vessels are being designed for bringing the waste carbon to locations for rock face injection, a process by which carbon is captured and turned into rock. While this process has yet to be proven at scale and is an expensive solution, it is a step in the right direction.

- There is also a general opportunity for the maritime sector to support the growing offshore wind industry. Global offshore wind capacity has a potential compound annual growth rate of 18% from 2021-2026. The type of vessels needed, and operational know-how include wind turbine installation vessels and vessels servicing the offshore wind farms. It is likely that currently available assets will be replaced, or retrofitted, with technology that can utilize the energy source of the offshore wind farm to refuel/recharge.

Greenheart’s Perspective on Achievable Medium-Term Advances Towards Net Zero

Decarbonization will be achieved over the decades ahead due to several practical challenges: (i) developing future fuel technologies that are not available today in scale; (ii) transitioning to a global renewable fleet requires trillions of dollars of investment; (iii) the capacity of global shipyards is finite and replacing existing tonnage would be highly energy intensive and far from the resourceful solution. That said, as the industry looks to advance its longer-term emissions goals, we expect there to be a phased approach to investment in research and development that will be transformative to the industry’s carbon footprint.

On the horizon, Hayfin believes that certain offerings are more achievable and realistic, including:

Dual-Fuel Engines: Increased adoption of dual-fuel technology including LNG, LPG, Methanol, and Bio-fuel (retrofittable) reduces CO2 emissions by up to 30% against current fuels.

Retrofit Options: Improvements and expansion of available retrofit options including fuel-saving devices, energy reduction systems, and vessel design optimization.

Ammonia: Increased adoption of ammonia as an alternative fuel source.

Operational improvement: Operational improvements both at the asset level and throughout the supply chain. An eventual transition to modular shipbuilding, whereby an asset owner can re-use / re-purpose key elements of a vessel to reduce the overall carbon impact of shipbuilding. This adjustment would increase accessibility to core components, such as the vessel’s engine, allowing for improved operating efficiencies (similar to aviation engine leasing and aircraft engine refurbishment, both models work in parallel to enable the latest technologies to be retrofitted onto older assets).

Circular Economy, Modular Ship Design, and Engine Leasing

- A circular economy is a production model which reduces waste by recovering resources at the end of a product’s life, feeding them back into production while creating an environmental benefit. The shipping industry has unique forms of circularity that can support the decarbonization journey. Long life assets

with regulated maintenance, practices ensure key vessel components can be reused and their life cycle extended. - Reuse and recycle concepts can be integrated into the design of future vessels, reducing the overall carbon impact of shipbuilding and operations.

- The industry has ambitious goals for modular vessels. The hull and other parts of the vessel are expected to last much longer than the current 25 years life expectancy. Certain sections of the vessel could then be replaced with new modules but reduce the need for the entire vessel to be recycled or become obsolete. The engine room is one of the obvious ‘modules’.

- Engine leasing is a concept widely adopted in the aviation sector. This results in easier and faster incorporation of new technology with manufacturers leasing out equipment. Efficiency is improved by accumulating engine knowledge and expertise in certain entities that can improve overall operating efficiencies and lower costs. It would require the complete re-design of ships to improve engine accessibility.

- Circularity also means enhanced collaboration: the green corridor initiative is a good example of getting all stakeholders involved with everyone from the exchange of knowledge, shared costs, and agreed goals.

Regulatory Push Driving Change

Heightened focus on decarbonisation will dramatically impact global regulation and policies. Along with accords such as the Paris Agreement of 2015 and recent announcements by the world’s largest economies pledging carbon neutrality by 2050, there are significant implications across sectors and geographies – including maritime.

Green Corridors

- The November 2021 COP26 conference saw over 20 nations agree to the establishment of green shipping corridors, zero-emission maritime routes between two or more ports, and importantly the development of infrastructure designed to enable the use of alternative fuels and green operating practices around port networks within these trading zones.

- The ambition is to have at least six green corridors by 2025 with the first Zero Emission Vessel operating in the corridors by this date and achieving 5% clean fuels used in shipping by 2030. This is expected to lay the foundation for the scale-up required beyond 2030.

- Viewed as a springboard from ambition to action, green corridors will create environments in which to test emerging technologies and lower development costs. Investments in fuel infrastructure on one corridor could remove uncertainty around zero-emission fuel supply availability in others and facilitate decarbonization in other industry sectors.

- Studies have been commissioned on trade-specific routes across 1) the Australia-Japan iron ore corridor, 2) the Asia-Europe container route, and 3) the Korea-Japan-US pure car carrier corridor. Altered supply chains based on specific corridor logic, political issues, or shorter distances traveled could lead to a change in the optimal size of vessels.

- Reducing the global scale of the challenge and applying logic to specific trade routes is seen as an efficient way to engage directly with key stakeholders across the value chain and to align on corridor-level consensus on fuel pathways, and policy support to help close the cost gap for higher-cost, zero-emission fuels and value-chain initiatives to pool end-user demand.

Carbon Pricing and Tax

- Leading ship owners and charterers are becoming increasingly vocal in support of a carbon tax as the clear financial incentive that is needed to encourage meaningful investment in maritime assets with alternative propulsion.

- The IMO has moved a step closer to creating a market-based measure, a financial mechanism to force shipping companies to make their vessels emit less GHG while providing potential funds for technology research and mitigation measures. The IMO also called for impact assessments to be done to show any possible effect of a carbon price on the shipping industry, one of the prerequisites for a measure.

- A number of discussions are underway on how to best apply and regulate the global carbon tax credit (IMO, US, and EU) and the pricing of this tax. A global solution is the ideal outcome.

Regulatory Incentive

- The mounting regulatory demands across the industry act as an incentive to build sizeable shipping platforms better aligned with end users and optimally positioned to capitalize on environmental challenges.

- By 2023, approximately 80% of the existing global fleet will need to adopt one or more of these measures in order to comply with IMO regulations.

- Energy Efficiency Existing Ship Index (EEXI) looks at the design of ships contracted prior to January 2013 and compares their energy efficiency to a benchmark. In terms of EEXI compliance, typical efficiency measures include propulsion and engine optimization as well as energy-efficient technologies and engine power limitation.

- Carbon Intensity Index (CII) will be used to determine the annual reduction factor needed to ensure continuous improvement of the ship’s operational carbon intensity within a specific rating level. Unlike ship design requirements (EEXI), the CII focuses on tracking emissions during operations. Specifically, the CII creates a standard to measure how efficiently a ship transports goods or passengers calculated in grams of CO2 emitted per cargo-carrying capacity and nautical mile and hence requires close collaboration between owners and charterers to optimize operations.

Key Takeaways

The path to decarbonization in shipping is complex and requires collaboration across the industry. In the short term, some supportive changes are materializing on the regulatory framework front, encouraging focus on fuel consumption and emissions. Stakeholders should encourage and support the best existing assets already on the water through both differentiation of income and collaboration on longer-term charter contracts in order to increase the visibility of these assets and encourage investment in retrofits and when feasible, new technologies.

Over the medium to long term, the industry is proactively defining the agenda itself, for example, via the development of green corridors and even through the introduction of self-imposed industry-wide carbon taxes. The end game would logically be an industry-wide propulsion solution for deep sea transportation infrastructure supported by massive infrastructure investment and buy-in by all stakeholders including ports, shipowners, yards/engine manufacturers, and charterers accelerating the industry’s path to net zero.

The ultimate ambition would be to see advances in manufacturing that could eventually lead to modular vessels built with green steel with zero emissions over a vessel’s full life cycle. In this vein, as in other industries, the real measure should not simply be daily emissions but rather the real comparison that measures the full lifecycle of the asset including the construction process and potential recycling.

Scale is becoming increasingly essential both for setting and leading the agenda. Credit strength and ESG compliance will be important factors when sharing the burden of the various new initiatives. Asset owner’s access to capital and contracts will be a progressively selective process and the marginal shipowner with their own technical management may, over time, become a relic of the past. The cooperation between stakeholders is likely to result in longer-term contracts providing investors and financiers better cash flow visibility for longer periods from strong credit counterparts.

For investors, these are welcome changes as the institutionalization of the maritime sector drives consolidation and growth of sizeable platforms that will increase the focus and prevalence of visible and predictable cash flow with a ‘value add infrastructure’ risk-reward profile. The maritime industry demands strategic engagement from the entire commercial ecosystem – both industry stakeholders and financial investors seeking to contribute towards tackling these ambitious targets that lie ahead.

The Maritime supply chain has historically remained a traditional industry and for investors, the current dynamic environment and unfolding transition is a unique opportunity for investors to drive change and achieve attractive returns.